M.M.A.D. (Mobile Mutually Assured Destruction) – Round 4

The great thing about the Cold War is that nobody actually nuked anyone for fear of reprisal , if only that kind of sense was shown by the scenario planners of the major mobile operators. When, I first discovered James Enck’s study of M.A.Dness in the fixed line sector a couple of years ago, I thought that the EU mobile markets with their relatively huge termination costs and even higher barriers to entry with prevent a similar game being played out here even with disruptive technology thrown into the equation.

How wrong I was!

The governments of EU have seemingly entered into some kind of termination race whilst at the same time the mobile operators have developed a strange kind of game which basically involves periodic slashing of prices.

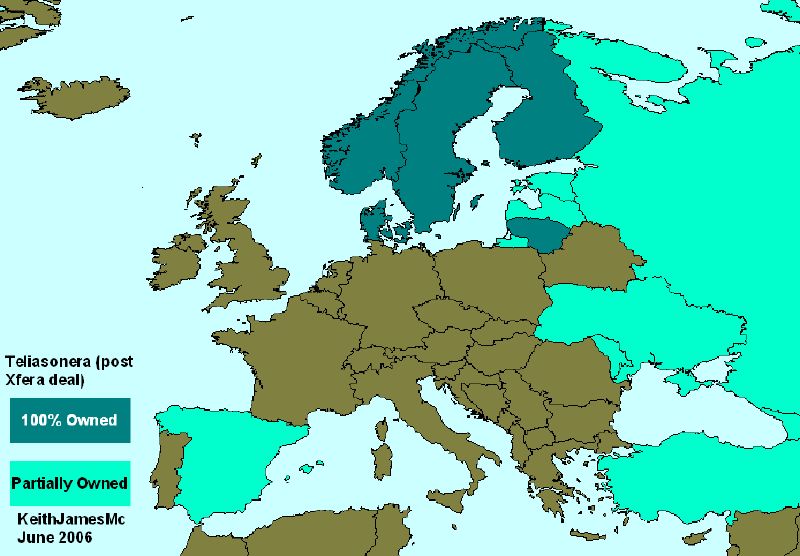

Today’s entry of Teliasonera into the Spanish market shows such utter stupidity that frankly I’m amazed that the shareholders are not in revolt already. Anyone will half-a-brain would think that Teliasonera would be thinking about re-building margin in Sweden and Finland and sorting out it’s long running partnership problems in Russia/CIS/Turkey. But, why do that when you can the Spanish and destroy the margins for everyone concerned?

Just to recap on Teliasonera’s expectations, they are basically initially paying €67m to increase its’ stake to 70% with a potential earn-out up to €270m. They also plan on investing (both opex + capex) €1bn over the next 5 years to take the company to Free Cash Flow positive. I presume Teliasonera’s share of this is 70%. They gave little details about the business plan apart from stating that they will follow the licence regulations (25% population coverage in Year 1), the economics have changed with the signing of National Roaming Agreement with Vodafone and the cost of the equipment has dramatically fallen over the last year. They straight-batted questions about the change of mood especially compared to previous comments about 3 Sweden (Spain is a different market) and the effect of entry of Saunalahti into Finland dropping Sonera’s margins from 40% to 20% (Spain is a different market and Teliasonera are a responsible operator not looking for quick exit). In other words it is a completely dubious venture at best – if this venture is Free Cash Flow positive in 5 years, I’ll eat my hat.

After the conference call, I'm still thinking perhaps it is just a huge game of bluff and Teliasonera really want Telefonica/Vodafone/Orange to pay them to go away. It is noticable that with VOD's exit from Sweden none of the 3 have operations in Teliasonera markets which can cause damage to the Teliasonera cash cows.

The new CEO of the Vodafone European Operations, Bill Morrow must be banging his head against the office wall. I wish I was good at Photoshop because I can just picture Oliver Hardy a.k.a Bill Morrow saying “That’s another fine mess, you got me into” to Stan Laurel a.k.a Arun Sarin.

A quick browse of the 2005/6 Vodafone Annual Report highlights just the type of problem he faces: assumptions in the financial model for the assessment of the write-off in Germany & Italy show the budgeted EBITDA growth over the next 5 years as 0.3% and -1.8% respectively. The only good thing I can possibly think of is that the price at buying out Verizon from Italy is going to go down in the future.

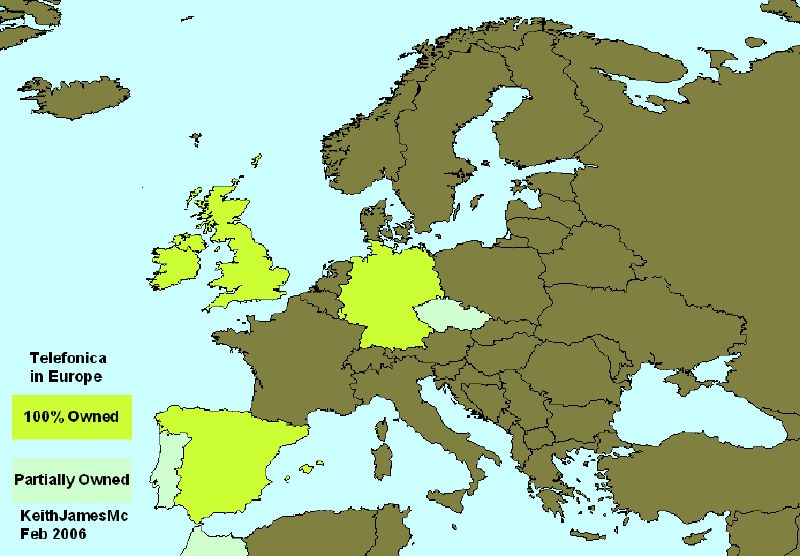

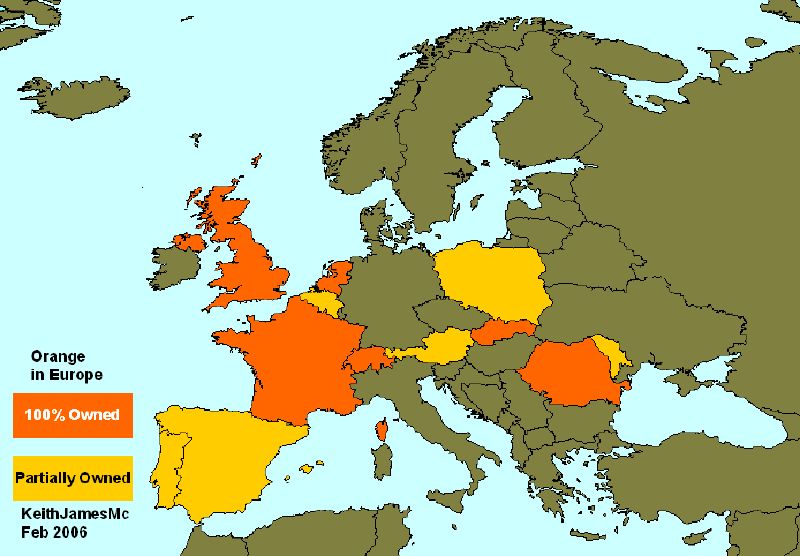

With a price war looming in 12 months in Spain with now both Orange and Teliasonera entering the market, I can only see EBIDTA going one way and with £10,571m of Spanish goodwill on the Balance Sheet, I fear that we can expect a Spanish goodwill write-off in the 3-5 year time frame. On the bright side, there is currently only £716m of goodwill on the UK Balance Sheet so far.

I expect the only end is sight is when the EU finally gets to regulate the prices across the whole of sector & manage the spectrum. I suppose then the economic rate of return will be approaching typical EU utility companies.

How wrong I was!

The governments of EU have seemingly entered into some kind of termination race whilst at the same time the mobile operators have developed a strange kind of game which basically involves periodic slashing of prices.

Today’s entry of Teliasonera into the Spanish market shows such utter stupidity that frankly I’m amazed that the shareholders are not in revolt already. Anyone will half-a-brain would think that Teliasonera would be thinking about re-building margin in Sweden and Finland and sorting out it’s long running partnership problems in Russia/CIS/Turkey. But, why do that when you can the Spanish and destroy the margins for everyone concerned?

Just to recap on Teliasonera’s expectations, they are basically initially paying €67m to increase its’ stake to 70% with a potential earn-out up to €270m. They also plan on investing (both opex + capex) €1bn over the next 5 years to take the company to Free Cash Flow positive. I presume Teliasonera’s share of this is 70%. They gave little details about the business plan apart from stating that they will follow the licence regulations (25% population coverage in Year 1), the economics have changed with the signing of National Roaming Agreement with Vodafone and the cost of the equipment has dramatically fallen over the last year. They straight-batted questions about the change of mood especially compared to previous comments about 3 Sweden (Spain is a different market) and the effect of entry of Saunalahti into Finland dropping Sonera’s margins from 40% to 20% (Spain is a different market and Teliasonera are a responsible operator not looking for quick exit). In other words it is a completely dubious venture at best – if this venture is Free Cash Flow positive in 5 years, I’ll eat my hat.

After the conference call, I'm still thinking perhaps it is just a huge game of bluff and Teliasonera really want Telefonica/Vodafone/Orange to pay them to go away. It is noticable that with VOD's exit from Sweden none of the 3 have operations in Teliasonera markets which can cause damage to the Teliasonera cash cows.

The new CEO of the Vodafone European Operations, Bill Morrow must be banging his head against the office wall. I wish I was good at Photoshop because I can just picture Oliver Hardy a.k.a Bill Morrow saying “That’s another fine mess, you got me into” to Stan Laurel a.k.a Arun Sarin.

A quick browse of the 2005/6 Vodafone Annual Report highlights just the type of problem he faces: assumptions in the financial model for the assessment of the write-off in Germany & Italy show the budgeted EBITDA growth over the next 5 years as 0.3% and -1.8% respectively. The only good thing I can possibly think of is that the price at buying out Verizon from Italy is going to go down in the future.

With a price war looming in 12 months in Spain with now both Orange and Teliasonera entering the market, I can only see EBIDTA going one way and with £10,571m of Spanish goodwill on the Balance Sheet, I fear that we can expect a Spanish goodwill write-off in the 3-5 year time frame. On the bright side, there is currently only £716m of goodwill on the UK Balance Sheet so far.

I expect the only end is sight is when the EU finally gets to regulate the prices across the whole of sector & manage the spectrum. I suppose then the economic rate of return will be approaching typical EU utility companies.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

<< Home