Spanish Gold

The o2 M&A team seem to be extremely busy at the moment. After yesterday’s purchase of Be Unlimited, today o2 have bought The Link for the miserly sum of £30m.

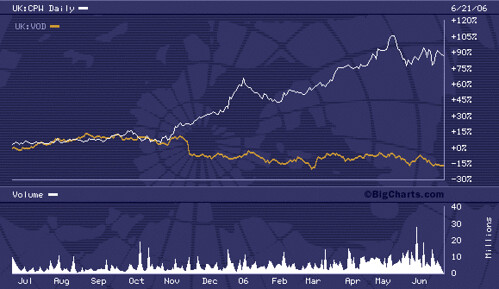

I know this is not going to win me any fans in the blogosphere, but I’m of the “Innovation is for show and Distribution is for dough” mentality. The acquisition of Be Unlimited is in the innovation category and will probably take a lot more investment to bear fruit, whereas the The Link acquisition is from the Distribution category and will provide a lot more immediate returns. I’m sure if the plan is executed correctly it will mean a short term transfer of value from Carphone Warehouse to Telefonica shareholders.

Carphone currently have a huge contract with o2 whereby they manage the o2 customers acquired via its’ own sales channel over the whole customer lifecycle providing billing and customer care functionality. This means that Carphone get a lot of recurring income from its’ o2 base. Carphone used to have a similar deal with Vodafone, but Vodafone cancelled the deal this year. The deal is really a throwback to a traditional Service Provider relationship. I don’t know whether o2 plan to cancel the contract at renewal time, but if they do it will cost Carphone a lot of money. Also, on the Carphone angle, why does o2 need Carphone now? For sure they are an extremely effective sales channel, but most of the Carphone publicity these days seems to be around the TalkTalk product set which competes directly with soon to be launched similar o2 products based around the acquired Be Unlimited capability. Even though, the Carphone share price has done wonders over the last 12 months, I would be seriously thinking now of reevaluating my positions.

Probably, the more important question is what do the o2 M&A team work on next? Personally, I would recommend a movement into the B2B mobile distribution game, strengthening o2 presence and sales capability. There are two juicy assets which would have any mobile CEO salivating: the first is Yes Telecom and the second is the mobile arm of Thus which has recently been acquired from Your Communications. The outstanding feature of both of these companies for o2 is not only their success but that they are huge distributors for Vodafone and therefore a purchase would be bring immediate market share benefits to o2.

I am of the school that the quickest route to improved profitability in the mobile business is simply through squeezing out the other players in the mobile value chain. The obvious candidates are the distributors since they are relatively weak. I also think the operators are using the Chinese manufacturers to squeeze margins out of the infrastructure providers and this is probably behind the mega-mergers which have happened in this space recently. I also think that any half decent mobile executive will be scheming how to reduce the take of the handset manufacturers and most importantly the taxman.

I know this is not going to win me any fans in the blogosphere, but I’m of the “Innovation is for show and Distribution is for dough” mentality. The acquisition of Be Unlimited is in the innovation category and will probably take a lot more investment to bear fruit, whereas the The Link acquisition is from the Distribution category and will provide a lot more immediate returns. I’m sure if the plan is executed correctly it will mean a short term transfer of value from Carphone Warehouse to Telefonica shareholders.

Carphone currently have a huge contract with o2 whereby they manage the o2 customers acquired via its’ own sales channel over the whole customer lifecycle providing billing and customer care functionality. This means that Carphone get a lot of recurring income from its’ o2 base. Carphone used to have a similar deal with Vodafone, but Vodafone cancelled the deal this year. The deal is really a throwback to a traditional Service Provider relationship. I don’t know whether o2 plan to cancel the contract at renewal time, but if they do it will cost Carphone a lot of money. Also, on the Carphone angle, why does o2 need Carphone now? For sure they are an extremely effective sales channel, but most of the Carphone publicity these days seems to be around the TalkTalk product set which competes directly with soon to be launched similar o2 products based around the acquired Be Unlimited capability. Even though, the Carphone share price has done wonders over the last 12 months, I would be seriously thinking now of reevaluating my positions.

Probably, the more important question is what do the o2 M&A team work on next? Personally, I would recommend a movement into the B2B mobile distribution game, strengthening o2 presence and sales capability. There are two juicy assets which would have any mobile CEO salivating: the first is Yes Telecom and the second is the mobile arm of Thus which has recently been acquired from Your Communications. The outstanding feature of both of these companies for o2 is not only their success but that they are huge distributors for Vodafone and therefore a purchase would be bring immediate market share benefits to o2.

I am of the school that the quickest route to improved profitability in the mobile business is simply through squeezing out the other players in the mobile value chain. The obvious candidates are the distributors since they are relatively weak. I also think the operators are using the Chinese manufacturers to squeeze margins out of the infrastructure providers and this is probably behind the mega-mergers which have happened in this space recently. I also think that any half decent mobile executive will be scheming how to reduce the take of the handset manufacturers and most importantly the taxman.

<< Home