Cellular in the Central European Markets

I’ve always been fascinated with Central Europe; primarily because when I was a youth the majority (excluding Austria and part of Germany) was behind a mysterious Iron Curtain and more recently due to the tragic break-up of Yugoslavia and the entrance of several countries into the EU club.

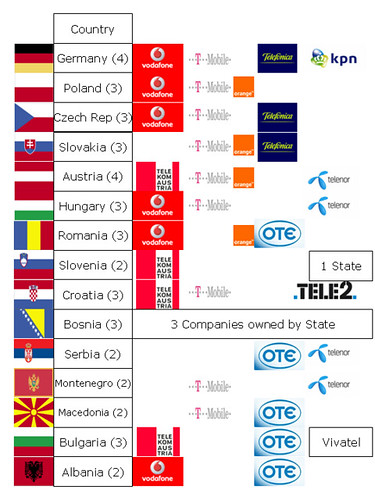

The large Cellular companies have wasted no time in taking large stakes within Central Europe. We have not quite reached the end-game but are getting quite close.

In a few countries the invasion of the Western Cellular Companies has not quite finished: Bosnia is due to sell its’ three state owned companies over the next 12 months; Slovenia still has to privatize its’ state-owned company; the third Bulgarian license, Vivatel is actually owned by the Icelandic company behind the infamous Saunalahti MVNO in Finland; and I can’t see any long term strategic reason for Tele2 holding a license in Croatia. I believe all of these licenses will be sold to the majors over the next couple of years to consolidate the Central European market further.

Also, there is a possibility of several countries licensing a third player: Slovenia, Serbia, Macedonia, Montenegro and Albania fall into this category.

I believe the final end game will be when the smaller regional players start selling out or making alliances will the larger players: we see this happening with Vodafone / Telekom Austria network partnership deal. I can quite easily envisage an environment where Telefónica and OTE do a similar network partnership deal to Vodafone/Telekom Austria.

Several of the big players such as Vodafone, Orange and T-Mobile face difficulties in taking control of several venture (eg Polkomtel) and squeezing out minorities. These problems I can see dragging out for several years.

As per normal, the wildcards are Orange and Telenor. I can’t see Orange being happy with its’ extremely weak position in the fastest growing part of Europe, but given that they are cash constrained at the moment their options are severely limited. An obvious solution to this difficulty is some sort of merger of Central European assets given the lack of overlap of properties: in Austria both own minority positions in the same operator, One. It is difficult to understand Telenor current strategy, so who knows what will happen.

The three key variables in looking at attractiveness of cellular markets are population, GDP and size of countries: Germany is by far and away the key market. A strong position in this market will pay for all sorts of expansion elsewhere.

<< Home