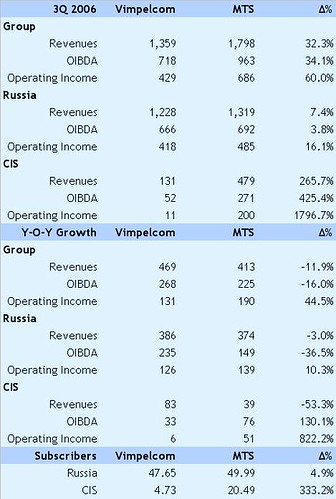

3Q2006: MTS vs Vimpelcom:

MTS (MBT) and Vimpelcom (VIP) have just released their 3Q results. They are both the clear market leaders in Russian cellular market and both are floated on the NYSE. Subscriber markets shares are MTS leading with 34.1%, Vimpelcom has 32.4%, the next largest operator is Megafon with 19.1% and the rest has 14.4%.

The main Russia market is probably already saturated with AC&M Consulting estimating that at the end of Sept, Russian market penetration is around 101% with 146.8m subscribers. This figure is vastly inflated with subscribers being defined as having activity within the last 6 months as opposed to 3 months which is the norm in Western Europe. Vimpelcom effectively admit that their figures are 8.86m too high or 22.8%. Even if this rate is repeated across the market and accounting for the predominately prepaid market and the use of duplicate SIM cards – there cannot be a lot of growth left in terms of actual “human” subscribers.

Year on Year Revenue and Profit growth is extremely healthy for both companies, although Vimpelcom is narrowing the gap on MTS. This is probably why MTS reshuffled its senior management in August bringing in people a lot more familiar with Western style marketing.

Future expansion for both is probably outside of Russia in the old CIS countries. Vimpelcom is leading the expansion charge with networks in Ukraine, Kazakhstan, Tajikistan, Uzbekistan, Georgia and Armenia; whereas MTS has networks in Ukraine, Uzbekistan, Turkmenistan and a 49% minority in Belarus.

Ukraine is the largest CIS market and MTS has a healthy 16.4m subscribers in the #2 operator ,UMC, earning US$415m revenues, OIBDA US$234m and Operating Income of US$174m. However, Vimpelcom has only recently launched and has a meager 0.9m subs, US$11.5 revenues and a loss at the OIBDA level of US6m and Operating Income of US$12.5m. The Ukrainian investment by Vimpelcom highlights the huge risk of investing in Russian Cellular. The main shareholders of Vimpelcom, Alfa Bank and Telenor are actually the joint owners of the market leader in the Ukraine, Kyivstar, and at face value it seems crazy for Vimpelcom to enter the market. It certainly has created a lot of fighting between the shareholders which is still not resolved to this day.

In Central Asia penetration is low and both companies have positions in the key market of Uzbekistan. Both are looking at expanding into all countries and recently had a real interesting brawl in Kyrgyzstan. In an unprecedented move the MTS founders have decided to reimburse the US$170m MTS seem to have lost in this unforgettable venture.

Both MTS and Vimpelcom were keen on expanding into the Caucasus and Vimpelcom has recently emerged winner of the early rounds purchasing assets in Georgia and Armenia. It will be interesting to see how much value these acquisitions bring in future reporting.

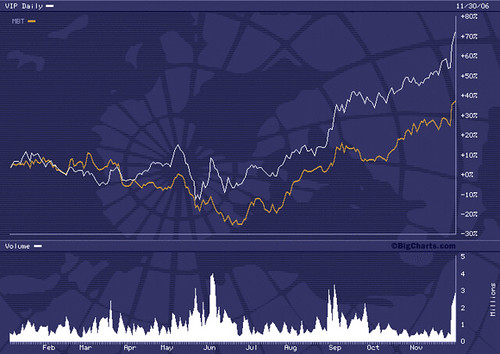

Both companies shares have performed extremely well in the previous quarter and I’m sure that part of the reason is that all major shareholders in Vimpelcom (Alfa and Telenor) and MTS (Sistema) are either buying shares directly or performing a share buyback programme.

I see very little operationally which will be a problem for either company, both will start generating large amounts of cashflow as the Russian markets saturate. The CIS will provide both companies will plenty of growth, albeit nowhere near as much as the recent growth in Russia.

The main problem with both is that it seems the owners want to merge the companies with Western companies. The MTS owner, Evtushenkov, is pushing for a merger with Deutsche Telekom who used to be a minority shareholder in MTS. The main owner of Vimpelcom, Fridman, is looking for a partner in the holding company, Altimo, for the Alfa group telecom assets. The MTS deal would be potentially quite clean; any Altimo deal would be horribly complex with minority positions in multiple assets who are fighting with their partners. A secondary problem is the real increase in political risk associated with Russia.

In summary, I feel that both are well performing companies with Vimpelcom probably currently slightly outperforming MTS. However, there are large risks of buying into the shares because the majority shareholders desires. They will be extremely interesting to watch over the next 12 months.

The main Russia market is probably already saturated with AC&M Consulting estimating that at the end of Sept, Russian market penetration is around 101% with 146.8m subscribers. This figure is vastly inflated with subscribers being defined as having activity within the last 6 months as opposed to 3 months which is the norm in Western Europe. Vimpelcom effectively admit that their figures are 8.86m too high or 22.8%. Even if this rate is repeated across the market and accounting for the predominately prepaid market and the use of duplicate SIM cards – there cannot be a lot of growth left in terms of actual “human” subscribers.

Year on Year Revenue and Profit growth is extremely healthy for both companies, although Vimpelcom is narrowing the gap on MTS. This is probably why MTS reshuffled its senior management in August bringing in people a lot more familiar with Western style marketing.

Future expansion for both is probably outside of Russia in the old CIS countries. Vimpelcom is leading the expansion charge with networks in Ukraine, Kazakhstan, Tajikistan, Uzbekistan, Georgia and Armenia; whereas MTS has networks in Ukraine, Uzbekistan, Turkmenistan and a 49% minority in Belarus.

Ukraine is the largest CIS market and MTS has a healthy 16.4m subscribers in the #2 operator ,UMC, earning US$415m revenues, OIBDA US$234m and Operating Income of US$174m. However, Vimpelcom has only recently launched and has a meager 0.9m subs, US$11.5 revenues and a loss at the OIBDA level of US6m and Operating Income of US$12.5m. The Ukrainian investment by Vimpelcom highlights the huge risk of investing in Russian Cellular. The main shareholders of Vimpelcom, Alfa Bank and Telenor are actually the joint owners of the market leader in the Ukraine, Kyivstar, and at face value it seems crazy for Vimpelcom to enter the market. It certainly has created a lot of fighting between the shareholders which is still not resolved to this day.

In Central Asia penetration is low and both companies have positions in the key market of Uzbekistan. Both are looking at expanding into all countries and recently had a real interesting brawl in Kyrgyzstan. In an unprecedented move the MTS founders have decided to reimburse the US$170m MTS seem to have lost in this unforgettable venture.

Both MTS and Vimpelcom were keen on expanding into the Caucasus and Vimpelcom has recently emerged winner of the early rounds purchasing assets in Georgia and Armenia. It will be interesting to see how much value these acquisitions bring in future reporting.

Both companies shares have performed extremely well in the previous quarter and I’m sure that part of the reason is that all major shareholders in Vimpelcom (Alfa and Telenor) and MTS (Sistema) are either buying shares directly or performing a share buyback programme.

I see very little operationally which will be a problem for either company, both will start generating large amounts of cashflow as the Russian markets saturate. The CIS will provide both companies will plenty of growth, albeit nowhere near as much as the recent growth in Russia.

The main problem with both is that it seems the owners want to merge the companies with Western companies. The MTS owner, Evtushenkov, is pushing for a merger with Deutsche Telekom who used to be a minority shareholder in MTS. The main owner of Vimpelcom, Fridman, is looking for a partner in the holding company, Altimo, for the Alfa group telecom assets. The MTS deal would be potentially quite clean; any Altimo deal would be horribly complex with minority positions in multiple assets who are fighting with their partners. A secondary problem is the real increase in political risk associated with Russia.

In summary, I feel that both are well performing companies with Vimpelcom probably currently slightly outperforming MTS. However, there are large risks of buying into the shares because the majority shareholders desires. They will be extremely interesting to watch over the next 12 months.